Esports betting affiliate marketing and a Barstool heat check

Opinion piece on how operators and affiliate groups can prepare to monetize the future of betting traffic + a check up on how Barstool's sportsbook product has performed since launch...

Every two weeks I write a piece on sports betting, gaming or trending themes in tech. If you would like to receive it directly in your inbox, subscribe now.

💰 Esports betting affiliate marketing: A sector that’s impossible to ignore

While sports betting affiliate M&A continues to be red hot in the US, I’d like to take a moment to look ahead to the next frontier of betting affiliate marketing. A couple months ago, I wrote a piece that covered the future of esports betting in the US, analyzing the Gen Z-driven growth trajectory, citing the success we’ve seen thus far in Europe and highlighting the segments and key stakeholders that undergird the ecosystem. However, one question that I posed in the piece, and left unanswered, was the implementation of affiliate marketing. My curiosity centered around how esports operators and affiliate groups such as Better Collective and Catena can implement effective affiliate marketing practices given the unique, tech-savvy consumer preferences of esports fans (e.g., penchant for live-streaming) and the decentralized nature of the space (i.e., individual creators/streamers are key stakeholders in esports). These aspects are somewhat divergent from traditional sports and worth exploring in more detail in order to create a framework for how to approach affiliate marketing as esports betting inevitably becomes more mainstream.

Whether it’s for traditional sports or esports, sportsbook affiliate partners play a vital role in the betting ecosystem, helping operators boost traffic and increase first-time depositors (FTDs). For every dollar in revenue a new online sportsbook generates, roughly 46% goes toward acquiring and retaining customers, research firm Eilers & Krejcik Gaming estimates. Within nascent markets, affiliates and operators typically work off a CPA structure in which affiliates receive fees in exchange for each FTD they generate for a respective operator. Building an efficient mouse trap is key for affiliates as their revenue depends on their ability to drive fan behavior. In traditional sports betting, this is typically achieved by providing education, original content, betting intelligence (i.e., stats) or social engagement to prospective bettors. In order to better understand how these four pillars are further evolving within esports betting affiliate marketing, I’ve put together a series of case studies that analyzes how the world’s largest affiliate groups and esports operators are set up to monetize the betting traffic of the future.

Affiliate Group Case Studies

As a reminder, affiliate groups are companies that pool together individual affiliate assets into a unified portfolio to create performance efficiencies and economies of scale for partnering sportsbook operators. The following affiliate group case studies are interesting because the selected two companies took distinctly different paths in setting up an esports affiliate asset within their portfolios, both having their own unique merits and target markets. However, the one theme that’s ubiquitous across the two assets is the importance of live-stream features.

Better Collective:

RakeTech:

In terms of takeaways for affiliate groups, these case studies provide precedence for acquiring or building publisher-like assets that offer a mix of location/language-dynamic news, tournament guides, betting intelligence and most importantly, live-stream features.

As mentioned earlier, the two companies highlighted above offer these features in distinctly different approaches. Better Collective specifically focuses on the CS:GO community while RakeTech prioritizes multi-title accessibility. I’d expect most affiliate groups to take the latter approach going forward given the scarcity of comparable, ultra high-quality assets specific to a hyper-engaged community like HLTV.org.

It’s worth noting that affiliate group leader Catena also has a handful of esports assets. Catena’s esports portfolio is highlighted by esportsbets.com, which is an in-house built esports affiliate asset that leveraged components from bolt-on acquisitions that Catena made in 2016 and 2017. Esportsbets.com is designed very similarly to traditional sports betting affiliate assets, offering sportsbook reviews, odds, news and schedules, but lacking any live-stream capabilities.

Lastly, as ‘bet on yourself’ markets continue to gain in popularity, stats/personal coach apps like blitz.gg and op.gg that provide personalized performance analysis and in-game overlays could function as great lead-gen assets for the esports operators who offer those markets (e.g., Unikrn).

Operator Case Studies

Betway:

BOA Gaming:

In terms of esports operator takeaways, partnering with affiliate groups like Better Collective and RakeTech to generate traffic and FTDs is table stakes. Additionally, the operator-specific case studies above provide precedence for alternate channels, such as influencer marketing and free-to-play (F2P) experiences, that esports operators can tap to broaden their reach.

Partnering with content creators to co-stream on operator-specific channels is a great way to leverage influence to drive engagement, education and FTDs. However, there is some red tape around this channel as countries in Europe such as the UK, France and Germany crack down on the use of celebrities and influencers within affiliate marketing.

Utilizing F2P is also a worthwhile approach that can benefit esports operators, whether it’s via integrating with F2P infrastructure or via acquiring an individual F2P platform. In terms of the former, BOA’s partnership with Sportsflare to power its F2P infrastructure for esports is a great example of this. I caught up with Sportsflare’s Founder & CPO Kenny Jang who provided the following thoughts on the potential of F2P within esports:

“I don't believe F2P is being well utilised yet, but should be picking up in the next few years as it's such a great customer acquisition tool.”

With the growing number of F2P and real-money esports fantasy platforms popping up in the US (e.g., ThriveFantasy, BallStreetTrading), it will be interesting to see if any operators explore a Bally’s/Monkey Knife Fight type deal as esports betting legalization eases across states and adoption/handle increases over the next decade. This type of inorganic growth would provide operators with an easy first database of high-quality users.

For those still skeptical of the growing wave of esports fans, which will inevitably cross-pollinate esports betting activity, I’ll leave you with this graphic that depicts both sports and esports team fandom amongst US male teens - of which esports organizations hold 2 of the top-3 positions.

🪑 Barstool checkup as NFL approaches

Earlier this year, I wrote a piece that covered Barstool’s sportsbook launch in Michigan which was significant because it represented the first time that Barstool launched concurrently with competitors in a state. Prior to entering the Michigan market, which legalized mobile and retail sports betting in January 2021, Barstool had only entered the crowded, established Pennsylvania market last September - two years after the state went live in 2018.

The initial results in Michigan were incredibly encouraging, making Penn’s customer acquisition strategy of leveraging Barstool’s cult-like following and original content as a lead-gen funnel look genius. Over the first 10 days of legalized sports betting in Michigan, operators excluding Barstool paid 136% of Gross Gaming Revenue (GGR) in promotional bonuses to acquire customers in the post-launch land grab. Barstool paid meaningfully less (~33% of GGR) because they had a differentiated media play that decreased their reliance on sign-up bonuses to get users into their funnel.

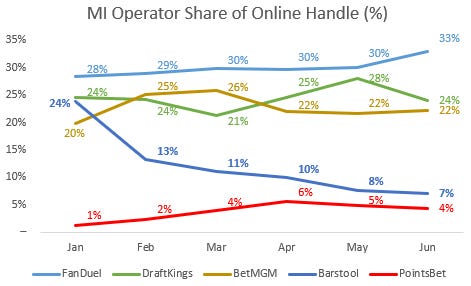

At the time, I left the aspect of Barstool's player retention and product innovation open ended given the lack of statistically significant data. However, fast forward six months to today and we have data to work off of. Unfortunately for Barstool, the narrative is one of underperformance. Since Barstool’s opening splash in January in which it saw itself rank in the top-3 of MI handle market share (only behind DraftKings and FanDuel), the operator’s share of total handle has dropped in each subsequent month.

And that’s despite an uptick in bonusing in February (Superbowl) and April (opening month of MLB) relative to its typical spend, measured as a percentage of GGR.

A similar theme of falling market share despite an uptick in bonusing (this time relative to the field) is also occurring within Pennsylvania where Barstool was recently eclipsed by BetMGM, which entered the PA market 3 months after Barstool in December 2020.

However, one aspect working in Barstool’s favor is its wide-array of parlay offerings, often constructed by their most popular personalities such as Big Cat and Dave Portnoy. The popularity of these influencer-driven offerings, which are significantly more risky than single game bets, helps to drive Barstool’s hold to higher levels relative to the rest of the field. Explained another way, higher-risk bets like parlays increase the chances of sportsbooks winning and taking your money. As a result, the hold, or the percentage of money that sportsbooks keep for every dollar wagered, for an operator with a larger proportion of parlays will be higher.

While the strategy of sports media properties as customer acquisition vehicles has been en vogue recently, the market is indicating that operators need additional innovation to retain customers beyond the initial deposit and to maintain share of handle leadership. FanDuel is undoubtedly succeeding in the current land grab because of its legacy funded DFS accounts that double as high-quality FTD leads as states go live. However, FanDuel’s ability to sustain and even increase its share of handle in some states is a testament to its best-in-class app UX. Eilers & Krejcik periodically publishes the results of its U.S. sports betting app performance review and to no surprise, FanDuel has time after time ranked as the best-performing app in their testing. The research firm recently stated:

“FanDuel, yet again, was the best-performing app in our 31-app testing universe. FanDuel’s app simply did everything well, and its seamlessly integrated same-game parlay product continued to resonate with our testers.”

As we approach the upcoming NFL season, it will be interesting to watch how the operator landscape shakes out as they compete to monetize the golden goose of US betting. With the expected launch of sports betting in states such as Arizona and Maryland (both of which Barstool has secured market access in) in the Fall, keep an eye out not only for how Barstool leverages its strong brand to drive customer acquisition out of the gate, but also for any in-app product innovation or loyalty-related features they roll out in effort to sustain market share over time.